From: aditya rana

Date: Sat, Jun 21, 2014 at 12:51 PM

Subject: On the "New Neutral"; Eat Food, Not Too Much, Mostly Plants-Conclusion!

Hi!,

The outlook for real interest rates is a key element which drives economies and markets, and Bill Gross, CIO of PIMCO, provides an insightful look into "The New Neutral" world in his latest monthly outlook which encapsulates a low real rate environment for years to come. To summarise:

-The Fed’s (and other central bank’s) policy rate, known as the feds funds ("FF") rate, is the foundation for the pricing of all risk assets and movements in the rate eventually results in the re-pricing of risk assets.

-The short term "real" (i.e. net of inflation) FF rate depends on GDP growth, productivity and a number of other factors in addition to inflationary expectations.

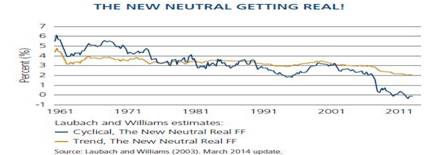

-Real rates have been in a long-term downtrend, with "trend" real rates having declined from over 4% in the early ’70s to below 2% today. The cyclical real rate today is actually -0.25%.

-A neutral rate is what is defined as the rate consistent with full employment trend growth and constant prices – described in the words of Janet Yellen as a "Goldilocks rate" – i.e. not too hot or not too cold and "just right".

-While the neutral real rate is dependent on a host of traditional factors like fiscal policy, trend growth rate of the global economy, housing prices, equity markets and the yield curve – there are two other structural factors which also play a key role:

-Since the trend growth rate has a significant impact on the neutral real rate, demographic and technological changes are important to consider since GDP growth is the sum of growth in the labour force and productivity. A slowing labour force growth with declining participation has likely lowered the neutral real rate by about 1%, as the data seems to corroborate.

-Another important factor which has an impact on the neutral real rate is the extent of financial leverage in the system, though it is difficult to quantify this relationship. A possible explanation could lie in the fact that a highly leveraged system results in trillions of "new cash" in the form of overnight repo, Fed Funds, credit cards etc, which are related to the financial rather than the real economy, and should therefore carry a zero (or close to zero) interest rate like ordinary cash.

-A related point is that a highly levered economy requires a low real rate to prevent a Lehman-type shock and maintain prosperity in the economy. History provides us with supporting data – during previous periods of high leverage like from ’45-’82 in the US and UK, real policy rates averaged -0.31% and -1.33% respectively. Other developed countries in Europe and Japan had even lower real rates.

-More recently, Japan provides further evidence of this important relationship between high leverage and low neutral real rates – which have been mildly positive due to deflation rather than the unwillingness of the BOJ to keep the FF rate at near zero. Going forward expect 0-0.50% neutral real rates in the US and even lower in other developed countries.

-The investment implications of the "New Neutral" are negative for savers who effectively are being taxed for the benefit of debtors. Specifically, it supports current level asset prices which appear to be less bubbly. In addition, generating income through credit, yield curve and currencies would be appropriate strategies.

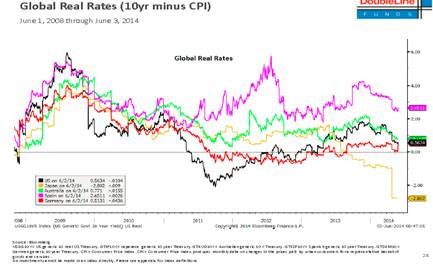

An insightful piece which has important implications for asset portfolio compositions over the next 3 to 5 years. To illustrate the importance of real rates for stock prices, please look at the chart below which plots the level of real rates across countries since 2008. No surprises that the country with the most significant fall in real yields, the US in 2011, also had the best performing stock market in subsequent years (until late last year).

-In the current central bank driven liquidity environment, it would be sensible to keep a well diversified portfolio of risk assets including equities, credit bonds and commodities.

-Given the relative outperformance of the US in recent years, it might be prudent to underweight the US relative to Europe (in particular the peripheral countries), Japan (which is likely to enter its next upside phase in the coming months following further policy easing and equity buying by domestic investors) and Emerging Markets (China, India, Brazil, Russia, Turkey, Thailand)- implemented through funds and sector/country ETFs. As the chart below illustrates, EM stocks have been in a sideways range from late 2011 and are poised to make an upside break.

-Regarding bond allocations – a core portfolio comprising high yield bond funds in Europe (and less so in the US), EM local currency bond funds, and a diversified portfolio of single high yield EM credit bonds (China, India, Brazil) and perhaps even some stressed EM sovereign positions (not for the faint hearted!).

-The time to perhaps start taking some risk of the table could come towards the end of the year, as we approach the period when the Fed is likely to signal a rate hike in 2015 (assuming the economy posts stronger growth for the 2nd and 3rd quarters). While this event is likely to initially shake global markets, it should not be a prolonged downturn as the market realises that the "New Neutral" implying a low level of real rates continues to be the fundamental theme for several more years.

Eat Food, Not too much, Mostly Plants – Conclusion:

To conclude the article written by the journalist Mike Pollan on the history of nutritionism in the US, I provide below a summary of his key rules of the thumb to guide you towards more healthy eating and living:

-Eat Whole Food: Eat what your great-grandmother would recognise as food – i.e. processed foods. Avoid products which are marketed bearing a variety for health claims – for example margarine was first touted as a health food to replace the traditional food, and it later turned out to cause heart attacks. Also avoid foods which contain numerous unfamiliar ingredients – especially those containing high fructose corn syrup.

-Eat less: While this is unwelcome advice, the scientific evidence in favour of eating less is compelling, showing slow aging in animals and many researchers believe that it is the most important dietary factor in preventing cancer. As the Okinawans used to say – "Hara Hachi Bu" -eat until you are 80% full.

-Eat mostly plants, especially leaves: While there may be scientific disagreement about why plants are healthy (antioxidants, fibre, omega-3s?), most scientists would agree that they are good for you. A plant-based diet also has less calories (except seeds) and it has been shown in various studies that vegetarians (and near vegetarians) are healthier than carnivores. As Thomas Jefferson advised – treat meat as a flavouring than a food.

-Eat traditional diets: Eat traditional diets – if they weren’t healthy the people who follow them would not be living today. Follow what as well how the food is eaten – small portions, no seconds and snacking, communal meals. "Let culture be your guide and not science".

-Learn to cook: The culture of the kitchen based on traditional diets contains more wisdom about diet and health than found today in nutrition journals. If possible, plant a garden.

-Diversify: Eat a broad variety of foods and species to get your nutrients.

Here’s to eating what your grandparents ate (with perhaps some minor tweaks!)

Comments

n how exactly these two topics are related????plz elaborate.....